Let me start with something I see all the time.

A physician walks into a meeting or an entrepreneur or a real estate investor running a seven-figure business. Sharp, Disciplined, Earning well above average and then we sit down and look at what they actually own… versus what they earn.

That’s where things start to feel off.

High income, Decent savings, a primary home with equity or maybe a retirement account they check once a year. And almost nothing that generates income without them.

According to Medscape’s 2024 Physician Wealth and Debt Report, 28% of physicians have a net worth under $500,000. Nearly half have less than $1 million.

This is while earning, on average, $374,000 per year. The math should work differently. It doesn’t because earning and building are not the same skill.

One is what they were trained for.The other… no one really teaches.

Pillar 2 – Financial Mastery doesn’t begin with investment tactics. It begins with a much more direct question:

Are you building an architecture or just sustaining an income stream?

“High income is not the same as wealth. A physician earning $400K a year with no tax strategy, no passive income, and no investment structure is not wealthy; they are income-dependent. That is a very comfortable treadmill.”

– Dr. Meetu Bhatnagar, Ph.D., CCIM

THE DATA — WHAT IS ACTUALLY HAPPENING

The Uncomfortable Numbers Most High Earners Ignore

Before strategy, there has to be clarity. Because if you don’t see the problem clearly, no strategy really works.

Here is the reality:

- 28% of physicians earning ~$374K/year have a net worth under $500K

- ~40% of their net worth is tied up in their primary residence, an illiquid, non-income-producing asset

- 9.5% is the long-term average annual return of commercial real estate

- 100% of most physicians’ income is active

That last number matters most. If 100% of your income depends on your time, your presence, and your ability to work, you don’t have a wealth position.

You have a high-income dependency.

Which means:

- One disruption resets progress

- One burnout phase slows everything

- One life event changes the equation

And the interesting part?

The people who move past this aren’t always earning more. They’re just structuring differently.

THE FRAMEWORK

The Three Shifts That Separate High Earners From Wealth Builders

Most high earners are not lacking effort. They’re just operating from a different mental model and that model quietly shapes everything.

Shift 1: From Income Focus to Asset Focus

Most people are focused on earning more. Wealth builders are focused on owning more.

An income-focused mindset asks: How do I increase my earnings?

An asset-focused mindset asks: How do I acquire assets that generate income without my involvement?

That difference sounds simple but it changes everything. Income needs your time. Assets don’t.

Every dollar that moves into an income-producing asset reduces future dependence on your schedule.

Shift 2: From Net Income to Net Worth Architecture

Your paycheck is not your wealth metric. Your productive net worth is.

The house you live in may have value but it doesn’t generate income.

Wealth builders look at:

- What portion of their net worth is working

- What is compounding

- What is actually producing cash flow

For most high earners, the first time they calculate this… it’s a wake-up call.

Shift 3: From Passive Tax Compliance to Active Tax Strategy

Taxes are the largest wealth drain for high earners. Larger than bad investments. Larger than market corrections. And yet, most professionals treat taxes as a once-a-year event.

In reality, it’s a year-round strategy. At a 37% federal tax rate and higher when state taxes are included, a significant portion of income is lost before it has any chance to compound.

Real estate changes this equation, but only when used intentionally.

THE MECHANISM – COMMERCIAL REAL ESTATE AS FINANCIAL ARCHITECTURE

Why Commercial Real Estate Is the Wealth Vehicle Most Professionals Overlook

Let me be direct here. I am a CCIM. I’ve spent years inside commercial real estate.

And one pattern shows up again and again: When you look at people who’ve built long-term, diversified wealth commercial real estate is almost always part of the picture.

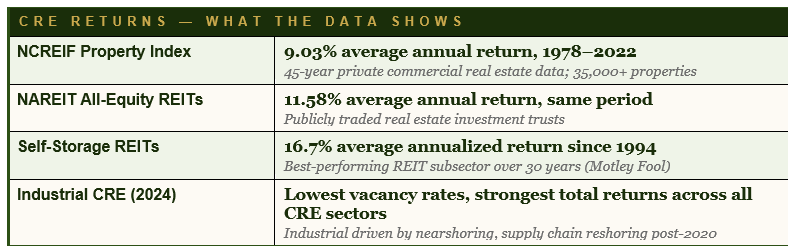

Here is the foundational data worth knowing:

But the return figures are not why commercial real estate belongs in a Financial Mastery conversation. Returns matter. What matters more is the unique tax structure that real estate investing unlocks – a structure that does not exist for any other asset class at this scale.

What makes real estate powerful is its structure:

- Cash flow

- Appreciation

- Leverage

- Depreciation

- Tax deferral

Very few asset classes combine all of these.

THE THREE TOOLS – WHAT EVERY HIGH EARNER SHOULD UNDERSTAND

Depreciation, the 1031 Exchange, and Cost Segregation

These are not advanced strategies. They are established, IRS-recognized tools. Most professionals just haven’t been shown how to use them.

Tool 1: Depreciation – The Paper Loss That Reduces Real Taxes

When you purchase a commercial property, the IRS allows you to deduct a portion of its value each year as depreciation, even if the property is increasing in value.

For commercial real estate, this is spread over 39 years. A $1M property generates roughly $25,641/year in deductions, reducing taxable income without any out-of-pocket expense.

For a physician in the 37% tax bracket, that’s about $9,487 in annual tax savings from depreciation alone. Over time, across multiple properties, these “paper losses” become a powerful tool for preserving wealth

Tool 2: Cost Segregation – Accelerating Depreciation into Year One

Instead of spreading deductions over 39 years, cost segregation breaks a property into components that can be depreciated over 5, 7, or 15 years.

The Tax Cuts and Jobs Act introduced bonus depreciation, which allowed immediate, first-year expensing of qualifying components. While bonus depreciation stood at 60% for properties placed in service in 2024, the One Big Beautiful Bill signed in 2025 reinstated 100% bonus depreciation for qualifying properties placed in service after January 19, 2025. Cost segregation studies have become significantly more powerful as a result.

The practical impact is meaningful. From Warren Averett’s published analysis: A $1M property could generate $255,432 in first-year deductions vs ~$30K under standard depreciation. At a 37% tax rate, that’s $83,000+ in tax savings in year one alone.

This dramatically improves early cash flow and reinvestment capacity.

Tool 3: The 1031 Exchange – Compounding Without the Tax Interruption

A 1031 exchange allows you to sell a property and reinvest the proceeds into another, without paying capital gains tax immediately.

Key rules:

- 45 days to identify replacement property

- 180 days to complete the transaction

- Funds held by a Qualified Intermediary

Example:

A property growing from $500K → $1M creates a $500K gain.

Without a 1031 → $100K–$150K lost to taxes

With a 1031 → full $1M continues compounding

Over time, this uninterrupted compounding significantly accelerates wealth.

Additionally, if held until death, heirs receive a step-up in basis, eliminating deferred gains, making this a cornerstone of long-term wealth transfer.

“Real estate is unique in its ability to defer capital gains taxes. The 1031 Exchange is a powerful tool that is especially valuable for high-net-worth individuals looking to preserve and grow their wealth through real estate.”

- Trinity Real Estate / Internal Revenue Code Section 1031

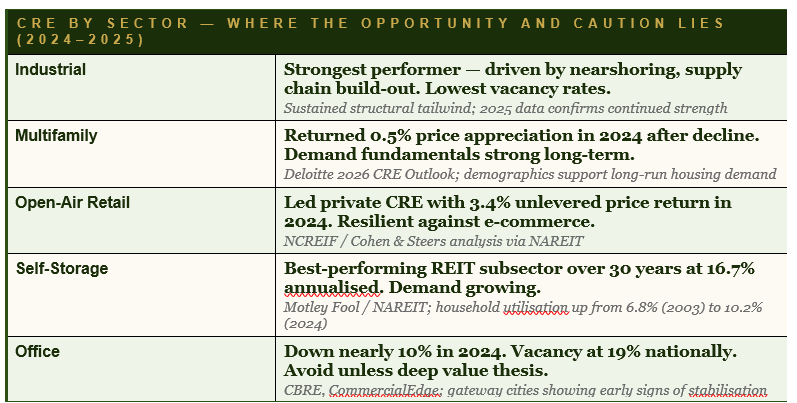

THE MARKET CONTEXT – WHAT IS HAPPENING RIGHT NOW

Where Commercial Real Estate Stands in 2025 and 2026

Commercial real estate has gone through a correction. Values peaked in early 2022 and declined by ~18% by mid-2024 (Green Street Index), with office vacancies reaching ~19% in some markets. There is real stress in parts of the market.

But this is also where opportunity shows up. Because experienced investors understand something simple: Institutions don’t buy at peaks. They accumulate during corrections.

And that’s exactly the phase we’ve been in.

According to Deloitte’s 2026 CRE Outlook, credit conditions are improving. Only 9% of banks were tightening lending standards by mid-2025, down from 30% in 2024 and 67% in 2023. Loan origination is also rising, up 13% since late 2024 and over 90% year-on-year.

This signals that the recovery window may be narrowing.

It doesn’t mean buying indiscriminately; it means investors who have prepared over the past 2–3 years are now positioned to act with clarity when the right opportunities emerge.

THE FRAMEWORK — HOW TO BUILD THE ARCHITECTURE

Financial Mastery Is Not a Product. It Is a System.

Here is the honest version of what Financial Mastery actually requires, not as a checklist, but as a way of thinking that I would want any Wealth Nation member to carry forward.

Step 1: Diagnose Before You Deploy

Before any investment, understand your full financial picture:

- Net worth (liquid, productive, illiquid, liabilities)

- Active vs passive income

- Effective vs statutory tax rate

These numbers reveal where your wealth structure is missing. Most high earners have never done this, yet it can be completed in a few hours with the right advisor. It’s one of the highest-return activities you can do.

Step 2: Tax Reduction Before Investment Return

Sequence matters. Tax strategy should come before investing.

Coordinated planning (depreciation, cost segregation, retirement accounts, entity structuring) can save $50K–$100K+ annually for high earners.

At 9% returns, $50K/year in tax savings = $2.7M+ over 20 years.

This isn’t about earning more; it’s about stopping the leak before compounding begins.

Step 3: Build the Income-Producing Asset Base

Wealth comes from assets that generate income without your presence.

Commercial real estate stands out because it combines:

- Cash flow

- Appreciation

- Tax advantages

- Leverage

But the principle matters more than the vehicle. Primary homes, cars, or collectibles are lifestyle assets, not wealth-building assets.

Step 4: Protect What You Build

Asset protection is essential. Holding significant assets personally exposes you to risk. Proper structures (LLCs, partnerships, trusts) create separation between your assets and liabilities.

This requires professional guidance, not DIY.

Step 5: Measure It

Track these quarterly:

- Net worth

- Passive income %

- Effective tax rate

- Portfolio returns

If passive income is increasing, your system is working. If not, the structure needs adjustment.

Wealth Nation, the professionals who build lasting financial independence do not earn more than everyone else – at least, not by a margin that explains the difference. They architect differently. They understand that a high income is the raw material, not the finished product. And they treat every dollar of that income as a decision point: does this dollar work for me, or does it work for someone else?

Build the architecture. The income is already there.